#MacroFriday: Central banks

It was a big week for central banks. On Wednesday and Thursday, monetary policy decisions were made by the Bank of Canada, Federal Reserve, Bank of Japan, Bank of England and the European Central Bank. We were particularly focused on their forward guidance against the backdrop of escalating tensions in Iran, given the implications for energy prices and the inflation outlook.

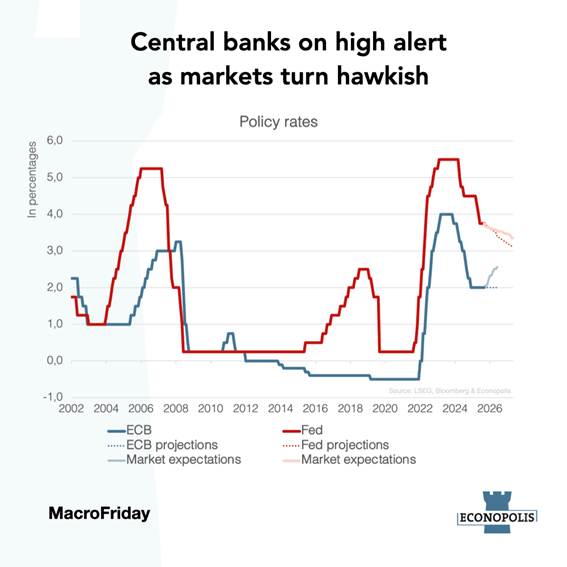

All these central banks kept interest rates unchanged compared to the previous meeting. Nevertheless, they all indicated that they were monitoring closely the shifting balance between economic activity and inflation. Risks to global growth are clearly tilted to the downside, while at the same time inflation risks have gone up due to higher energy prices. For now, most central banks continue to treat the energy shock as a one-off effect on inflation. That said, there is growing awareness that persistent energy price increases could trigger broader, second-round inflationary pressures. Inflation on the medium term will be heavily influenced by the intensity and duration of the conflict and on how energy prices affect consumer prices and the economy.

Market pricing has shifted notably in recent weeks, pointing to a more hawkish outlook than the current central bank guidance. Investors now expect the first Fed rate cut only beyond a one-year horizon, whereas the Fed continues to signal that one cut in 2026 remains plausible. In the euro area, markets are pricing in roughly two ECB rate hikes by October, in contrast with the ECB’s previous indication that rates are likely to remain near 2% through 2026. Having fallen behind the curve in 2022, policymakers are now more alert to the risk that sustained energy price increases could de-anchor inflation expectations and lead to second-round effects. This is why they have opted for a wait-and-see approach while remaining on high alert.