#MacroFriday: Private Credit

The sharp rise in interest rates since 2022 has tightened lending conditions through banks and public markets, pushing borrowers toward private credit as an alternative source of financing. Its appeal lies in speed, flexibility, and lighter regulatory constraints. Yet this shift is now being tested. Higher financing costs are exposing weaker borrowers, while lenders are turning more selective, reversing years of aggressive credit expansion.

Despite its rapid growth, private credit does not yet constitute a systemic risk to the financial system or the broader economy. The asset class sits largely outside the banking system and is funded predominantly by institutional investors, limiting classic contagion channels. However, recent episodes of gated or halted fund redemptions highlight a key vulnerability: liquidity mismatches can quickly turn sentiment into stress, which reinforces valuation pressures through self-fulfilling dynamics.

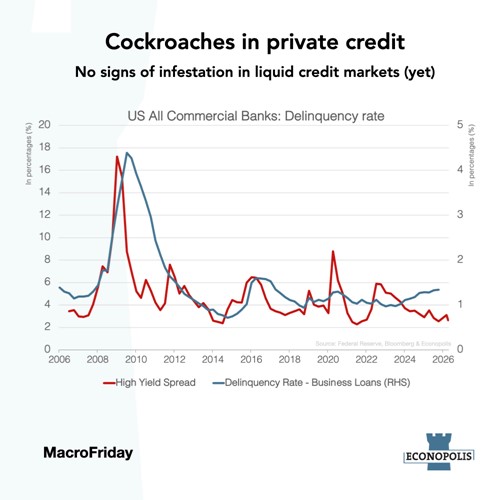

Nevertheless, delinquencies on bank business loans have been rising, but remain at low levels, while high-yield spreads are still compressed and do not signal a severe downturn. This suggests that financial markets are, for now, absorbing the shift in financial conditions and the stress in the liquid private credit market. However, if strains in illiquid private credit markets continue to build, they could eventually spill over into liquid markets and the real economy, primarily through a further tightening in credit availability.