Holdings companies have underperformed, yet we launch a fund focused on them?! Here’s why.

Despite outperforming the market over the long term, a lot of investors will have noticed that more recently, holding companies have underperformed the broader market. That feeling is correct as holding companies have returned 8,1% per annum between 2020 and 2025 whereas the MSCI World did more than 12%. Even though the returns of holding companies have not been terrible, they did however lag the index by more than 4 percentage points. This leaves us with some important questions like:

- Is the underperformance widespread?

- Has this always been the case?

- What are some of the catalysts that could turn the tide?

An even more important question is: “Why would Econopolis now want to launch a fund dedicated to this segment?” We will address each of these questions in the next few pages. All data is updated until 31/12/2025.

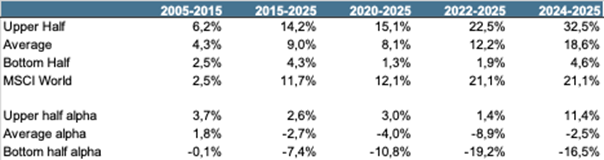

At Econopolis, we have one of the broadest databases on holding companies available with data on 70 global holdings going back more than 20 years. For this exercise, we will split up our collective of holding companies into two groups: the leaders and the chasers. The leaders are the upper half of companies with the best performance, and the chasers are the bottom half of companies with the poorest performance.

Our first conclusion is that the underperformance versus the MSCI World is not widespread, on the contrary, but instead concentrated with a few names that have fallen from grace. Some of these weak players include names like Kinnevik, VNV Global and even our own Belgian Quest for Growth. To give you an idea: over the last 5 years, the upper half returned 15,1% per annum and hereby beating the index comfortably. Yet, the bottom half returned only 1,3%!

This brings us to our second question: “Has this gap always been there?”

The logical answer would be: yes! Unfortunately, the opposite is true.

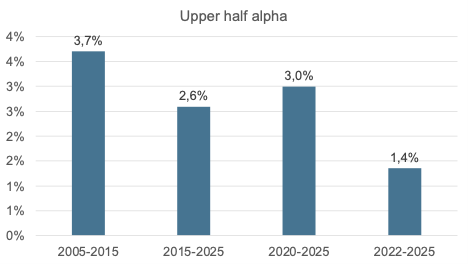

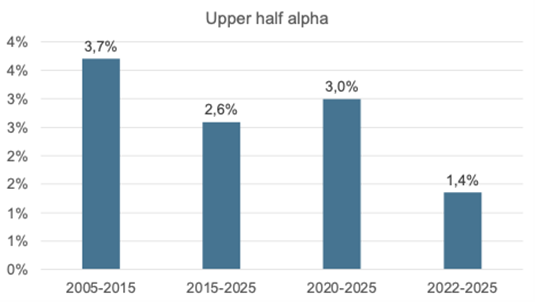

The upper half of our sample have consistently outperformed the MSCI World over each period. The annual alpha has ranged between 1,5-4% per annum.

Between 2005 and 2015, both groups (upper and bottom half) managed to beat the MSCI World. Holding companies as a whole outperformed the MSCI World by 1,8% per annum. Yet, over the last 10 years, the average of the whole sector has underperformed the index. As we have seen from the previous graph, this is not due to the leaders who have continued to generate significant alpha.

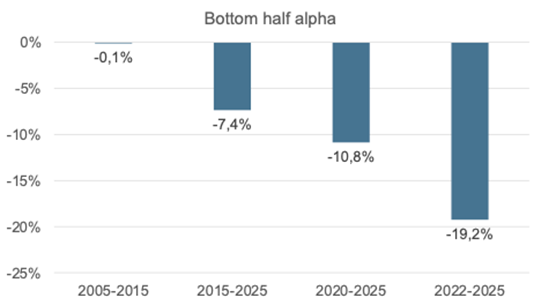

The answer lies in the performance of the bottom half which has deteriorated significantly. Whereas the bottom half performed relatively in line with the MSCI World between 2005 and 2015, they have underperformed by 7,4% per annum between 2015-2025. It gets worse. Over the last 3 years, the bottom half has performed 19,2% per year (!) worse than the index!

Some of the outliers here are Syncona, Kinnevik, VNV Global, Quest for Growth and Eurazeo. Coincidentally, all of them had to take serious impairments in the private asset part of their portfolios. Especially Kinnevik and VNV Global who are invested in venture capital-like assets saw their NAV skyrocket in 2021, only to see it fall down again in the years that followed. This article is not meant to be critical of private assets in the portfolios of investment companies as there are just as many companies that have benefited from their private assets over the last 3 years (think of Softbank, Scottish Mortgage, Seraphim, etc.) and there are many reasons why you would want to have private assets at holding companies. However, it does prove that investors should pay attention to the valuation of private assets and how these valuations have come about.

With all this being said, we can conclude that the best holding companies have continued to generate alpha and that the recent underperformance of holding companies is almost fully attributable to the deteriorating performance of the bottom half.

That also means that stock picking in holding companies has become evermore important. Whereas in the past, investors could simply buy the whole sector in order to achieve good returns, this is no longer possible today. It is for that reason that Joren Van Aken (specialized in holding companies) has recently joined our firm to manage the Econopolis Capital Allocators fund with the goal of capturing the names from the upper half in the fund.

That brings us to our final question: “What are some of the potential catalysts to turn the tide?”

There are a couple of reasons to be enthusiastic about the future performance of holding companies.

The first one is the number of IPOs that are expected in 2026. Think of the IPOs of SpaceX, OpenAI or Anthropic. SpaceX represents 15% of the portfolio of Scottish Mortgage Investment Trust (SMT). SMT has valued SpaceX at USD 800bn in its books. Yet, the media is arguing for an IPO valuation of USD 1,5 to 1,75 trillion, or double the amount at which SMT has SpaceX valued in its NAV. What the valuation of SpaceX will be in a few months, we do not know. However, what we do know is that if these rumors come to fruition that SMT will see an incredible uplift in its NAV. The same can be said for Sofina who through its Sofina Private Funds also has exposure to SpaceX but also to OpenAI and Anthropic.

A second element why we keep our conviction on holding companies is that there is often a family link. Why is that important? Patience.

A CEO of an investment company once told me: “We manage our holding like a Patek Philippe. We take care of it for the next generation.” This is exactly the right mindset for outperforming the market which inherently only looks out a few quarters into the future at best.

A lot of private equity firms claim to be long-term investors, yet the average holding period of a private equity firm is 5 to 7 years. That means that after this period they are looking for the exit, regardless if this is the right time to exit or not. To put this into perspective, the average holding period of Investor AB is more than 50 years. Talking about long-term!

This gap in horizon may proof to be an advantage for holding companies in the coming years as a lot of private equity firms will become forced sellers which may allow holding companies to pick up great companies on the cheap.

Finally, we want to highlight that holding companies themselves are quite cheap today. The average discount of the sector is nearly 30% which is quite a bit above the 20-year average of about 21%. A narrowing of the discount to more normalized levels may be a nice tailwind for the sector in the coming years.

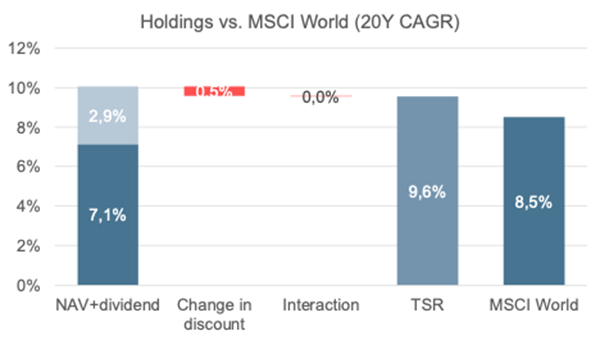

An important point of context is that we will never buy a holding company on the basis of its discount alone. That is because over longer periods of time, the growth of the NAV per share combined with dividends determine >90% of shareholder returns.

Bringing all of this together, we would like to highlight that we are launching a fund which will focus exclusively on holding companies.

We believe holdings companies have shown throughout multiple decades their ability to outperform the MSCI World by quite some margin and we aim to replicate that alpha in the fund. The fund’s goal is to identify the leaders within the sector and hold them for the long term. The fund will have a concentrated portfolio of 10-20 names with the goal of letting its winners compound over multiple years. How will we identify these winners? By focusing on the holding companies with:

- A clear strategy

- A strong track record or clear view on why track record will improve

- High levels of skin in the game

- Diversification at a low cost

- Access to unique assets

For more information, feel free to contact us.