Maxim Gilis obtained a Master in Applied Economics at the University of Antwerp in 2015. His master thesis examined the diversification of stocks in emerging markets. Next he obtained an additional Master of Finance at the Antwerp Management School, where he researched sustainable responsible investing for a European asset management company. He joined Econopolis in the summer of 2016.

The growing challenges in the commercial real estate sector for office spaces

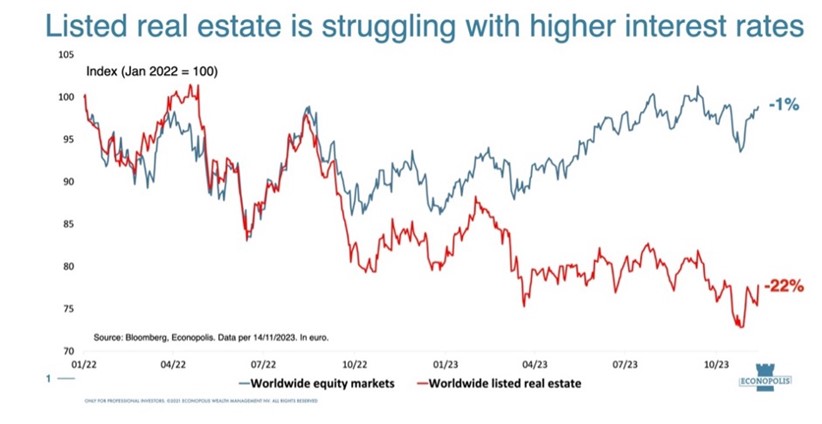

The recently published US inflation data, which came in lower than expected, has brought some relief to financial markets. As a result, interest rates declined while equity markets experienced a rise. The real estate sector, known for its high correlation with interest rates, greatly benefited from this trend, a pattern that has been evident over the past year. However, listed real estate suffered due to the shift in central bank policies. The era of cheap financing, which real estate companies enjoyed over the past decade, is fading away. This shift has led investors to worry that the golden age of real estate may have reached its conclusion.

Several segments of the real estate market are struggling with the fallout of covid-19. Retail looked like the segment that would suffer the most as e-commerce became even more popular. However, it is commercial real estate such as offices that are currently in the middle of the storm. Almost three years after the start of the covid-19 pandemic, working from home is here to stay. This of course has a huge impact on the office space that is needed and consequently, also on the valuation of offices.

According to Professor Stijn Van Nieuwerburgh, a New York resident working at the Columbia Business School, we are currently only in the early innings of the troubles for offices. Even though the pandemic is over, the return to office has been disappointing. According to Professor Van Nieuwerburgh, the pandemic has created a disconnect that is best explained in the words of Slack CEO and co-founder Stewart Butterfield, “work is no longer a place you go but something you do”. Recent data supports this statement. Physical office visits are only half of the pre-covid levels. More importantly, this number has been stable over the past year. Companies have also learned how to run their offices more efficiently, again reducing the need for office space. Albeit rising, vacancy in offices is currently still rather limited. One of the main reasons for this is the fact that many tenants still must decide what they will do with the office space that they rent, given the relatively long duration of their leases. Professor Van Nieuwerburgh expects many tenants to not renew their lease, at lower rent levels or only for a reduced size. Desk-sharing alone could for example lead to an average reduction of 10% in demand for office space by 2026 according to Savills, a real estate services company. Such a scenario would of course have an impact on the profitability of commercial real estate companies renting out office space.

Increased vacancy combined with higher interest rates would of course also impact the valuation of offices. Together with some colleagues, Professor Van Nieuwerburgh created a model to value offices. Mainly driven by working-from-home and higher interest rates, US offices could be worth 40-45% less than before covid-19. Offices of the highest quality (the so-called grade A+ offices or trophy buildings) would be able to limit losses to 20%, but some lower-tier offices could lose more than 60% in value. This is consistent with the flight-to-quality that we have observed recently in offices, creating even larger differences between the haves and the have-nots.

It is important to note that there are some differences between the US and Europe. The return-to-office is larger in Europa, although there are stark differences between countries. Vacancies in Europe have also risen, but to much lower levels than in the US. Consequently, rents in Europe have not declined as in the US. In fact, a key difference between the US and Europe is the fact that in latter rent levels are much more linked to inflation compared to the former.

The research of Professor Van Nieuwerburgh recently came to the attention of the media on the back of a possible scenario in one of his research papers, namely the urban doom loop. This does not necessarily fully reflect Professor Van Nieuwerburgh’s research, as it is only one of the possible outcomes, but of course doom sells. The urban doom loop entails that valuation losses on offices would lead to severe troubles for some US cities. For many of them, taxes on real estate are a main part of their budget. For example, in New York, real estate taxes are over 10% of the city’s revenues. In Boston or Dallas, it is even double. As offices would decline in value, tax revenues for these cities would decline. This would mean that these cities will have to compensate these revenue losses by either higher taxes and/or expenditure cuts on public services. This would drive away both employees and employers. Especially with working-from-home going mainstream, and Americans already being more mobile to relocate compared to Europeans. A vicious circle would be created because more people leaving a city, would again lead to less revenues for city budgets and so on. Europe is better prepared for the urban doom loop as European cities are better diversified. They are more focused on consumption and living compared to American cities which are mainly focused on production and work. Examples are Houston, Dallas or Chicago, which are at night rather empty.

The US banking sector is also vulnerable to the problems in offices real estate. Smaller, regional US banks have a lot of commercial (offices) real estate debt on its balance sheets. Large negative revaluations of offices, combined with high leverage, could thus create enormous losses for these banks. Offices are cyclical and defaults on loans are less frowned upon in the US compared to Europe. Currently, these banks are kicking the can down the road by granting loan extensions, hoping that these problems would be solved in the future by for example lower interest rates again. However, such zombie lending is not productive for the US economy, as it creates less room for loans to productive companies.

There are nevertheless solutions for the urban doom loop. According to Professor Van Nieuwerburgh, the fundamental issue is that there are too many offices in US cities. On the other hand, there is a lack of (affordable) residential buildings in these cities. The logical solution would thus be converting some of the redundant or obsolete (brown) offices stock to for example (green) apartments. This would create a triple win. In the Netherlands for example, circa 20% of new housing came from conversions. However, such conversion brings along some challenges. Only a small part of US offices is suitable to be converted easily to apartments because of amongst others building technicities. The government should support this process by providing tax breaks and zoning/building code reforms.

In sum, commercial real estate such as offices are challenged by hybrid or remote work, as well as higher interest rates and a possible economic slowdown. US offices, cities and banks are somewhat more challenged than their European counterparts. To avoid a so-called urban doom loop, (brown) offices would need to be converted to (green) apartments. It is important that the government provides the right incentives for this. Because the fundamental issue remains that there are just too many offices, especially when one factors in the rise of artificial intelligence, which would further reduce the need for office space.

About the author

Maxim Gilis

comments powered by Disqus